You’ll learn how to manage your savings through investments that are simple, cost-effective, and poised for long-term growth. You’ll also understand why it’s unwise to keep all savings exclusively as cash, bonds, and stocks. The authors will introduce and walk you through a formula, the Merton Share formula, to help identify an optimal balance between risky and safe assets in your portfolio and adjust it to changing economy.

R4GoodPersonalFinances

R package

R

RBloggers

asset allocation

investing

EDO

TIPS

ETF

Merton Share

Risk Adjusted Returns

Authors

Kamil Wais

Olesia Wais

Published

October 31, 2024

Modified

December 31, 2024

What will you learn from this article?

You will learn how to invest your savings in a manner that is:

simple (self-manageable with just two asset classes),

repeatable (applicable throughout your entire life),

efficient (protects your savings from inflation and allows for growth beyond inflation),

optimal (balances risk so it’s neither excessive nor insufficient).

You’ll dive into a strategy grounded in solid academic research, all set to boost your long-term living standards. With all the conflicting advice flying around (“invest here, invest there”), you’ll finally get a clear idea of how to handle your savings. And this isn’t just for now—it’s for any time down the road.

Tip

All calculations and plots in this article are done with the use of the functions from the R4GoodPersonalFinances R package:

Once we get a handle on our spending, and our income hits a comfortable level, we can start building up some savings. If we don’t need to dip into those savings right away, it’s time to think about our next long-term move. We can ask ourselves a question: Should we let our saving sit in cash or put it into bonds, stocks, or maybe a bit of both?

Why keeping all your savings in cash isn’t the best idea?

One way to handle our savings is by holding onto cash. However, with inflation chipping away at its buying power over time, it might not be as safe as it appears. When we choose not to invest, we are basically agreeing to let our buying power shrink over time, so we can afford less in the future.

Let’s consider a scenario where the yearly inflation rate is 2%, which aligns with the target inflation rate in the US and is below Poland’s target of 2.5%. Imagine you have $10, which you can use to buy 10 apples today. You decide to save this money in cash, intending to use it upon retiring in 30 years. When you finally retire and attempt to buy apples with the same $10, you’ll find your purchasing power has decreased due to inflation. Now, you can only purchase 5.5 apples. This simple example demonstrates how inflation can significantly affect your retirement savings and overall financial independence.

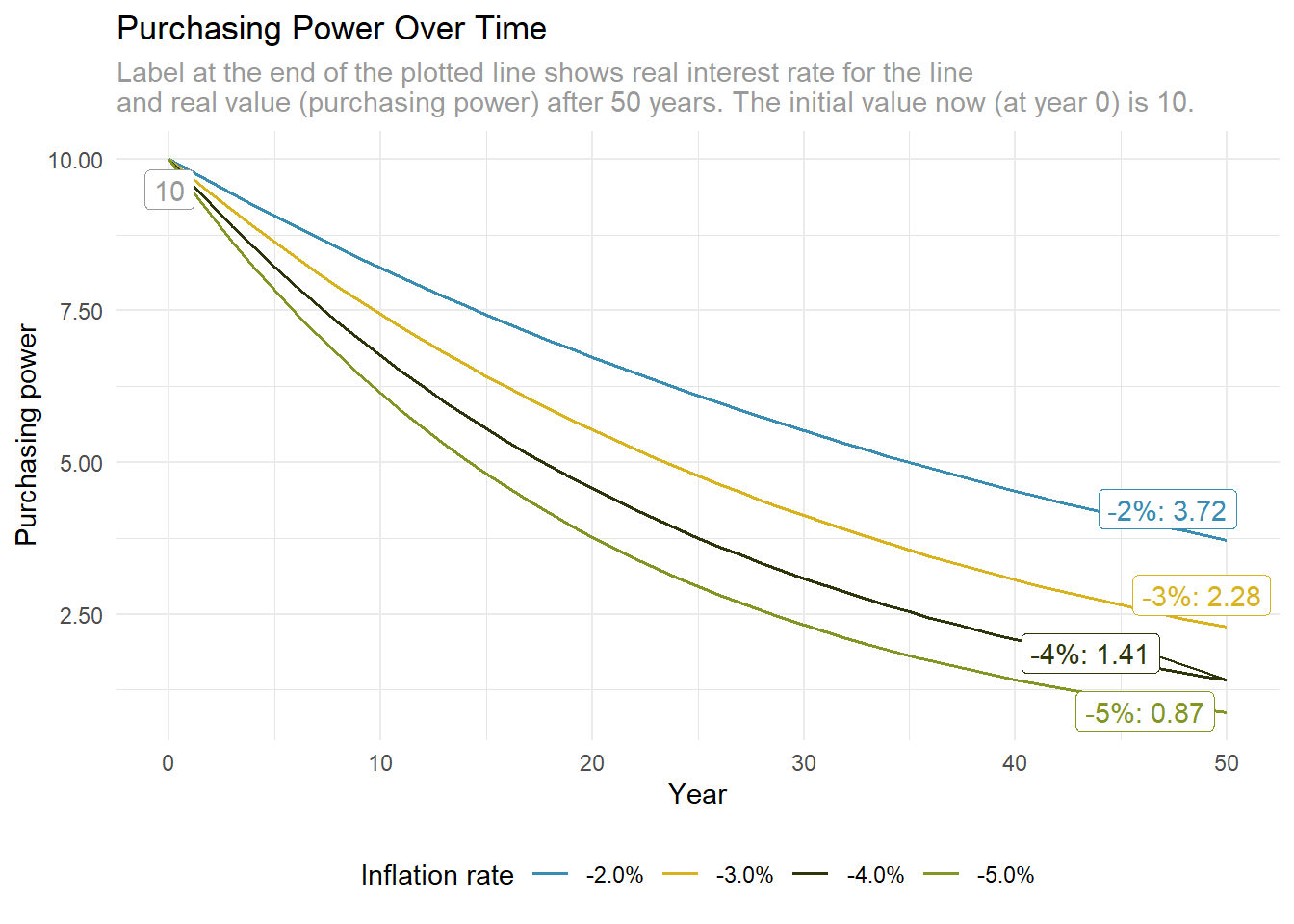

Please note that a yearly rate of 2% signifies a relatively low level of inflation. Over time, the effects of inflation become more apparent, especially when the rate is higher. Observe how rapidly the purchasing power of your $10 declines over time in the plot below. With an inflation rate of 2%, your savings will lose 50% of their purchasing power in 35 years. However, if the average annual inflation rate is 5%, they will lose the same 50% in just 14 years.

Code

plot_purchasing_power( x =10, real_interest_rate =seq(from =-0.02, to =-0.05, by =-0.01), legend_title ="Inflation rate")

Figure 1: The effect of inflation on the purchasing power over time.

It may be tempting to diversify your savings by investing in foreign currencies. However, it is crucial to acknowledge that the inflation rates tied to each individual currency will diminish their purchasing power over time.

Warning

If you keep your savings in cash, inflation will inevitably reduce your purchasing power over time.

If you stash all your savings in cash, it’s going to hurt your financial stability over time. To keep your money safe from inflation, you might want to think about putting it into secure investments like inflation-protected bonds. But should you really put all your savings into bonds?

Why you should not invest solely in bonds?

Investing in bonds is actually quite reasonable when considering inflation-protected bonds. In the U.S., options like Treasury Inflation-Protected Securities (TIPS) or limited Series I Savings Bonds are available.1 In Poland, individuals can opt for 10-year inflation-protected bonds such as EDO, as well as limited 12-year ROD bonds.2

At the time of writing this post, Polish EDO bonds offer 6.55% in the first year, and a fixed interest rate of 2.00% above inflation in the next 9 years.3 In comparison, Series I Savings Bonds offer a 4.28% interest rate, which includes a fixed rate of 1.30% above the inflation.4

The 2.00% fixed rate for EDO is relatively high, especially when compared to its previous rate of 1.50%, which was more aligned with the current US I Savings Bonds. When evaluating the 2% real interest rate above inflation, we must assess whether it is substantial enough to merit our consideration, or does it fall short of our expectations?

Let’s attempt to answer this question by unusually beginning with a reference to a minor footnote found in the book Missing Billionaires:

In the early days of the TIPS market in 1999, when they offered a yield of around 4%, Warren Buffet’s Berkshire Hathaway was one of the largest buyers, and he reportedly said that he’d be willing to replace his entire portfolio of risky assets with these long-term US Treasury bonds with a guaranteed return of 4% above inflation. At the time, the TIPS market was not big and liquid enough for him to act on this view, and yields on TIPS dropped sharply by the end of 2000 (Haghani and White 2023, 234).

That’s interesting! Warren Buffet would consider investing entirely in bonds if the real interest rate reaches 4%. However, our 2% yield from EDO bonds seems less competitive. In early 2016, the authors of the Missing Billionaires surveyed 60 friends and colleagues from the financial industry, primarily high-net-worth taxable U.S. investors. They asked what risk-free, inflation-protected, after-tax return they would accept to permanently forgo all other investment opportunities. The average response was about 2.5% (Haghani and White 2023, 233). For many wealthy individuals, even a 2% real interest rate may be sufficient, provided their spending isn’t excessively high. But how is this possible? It’s all thanks to compound interest!

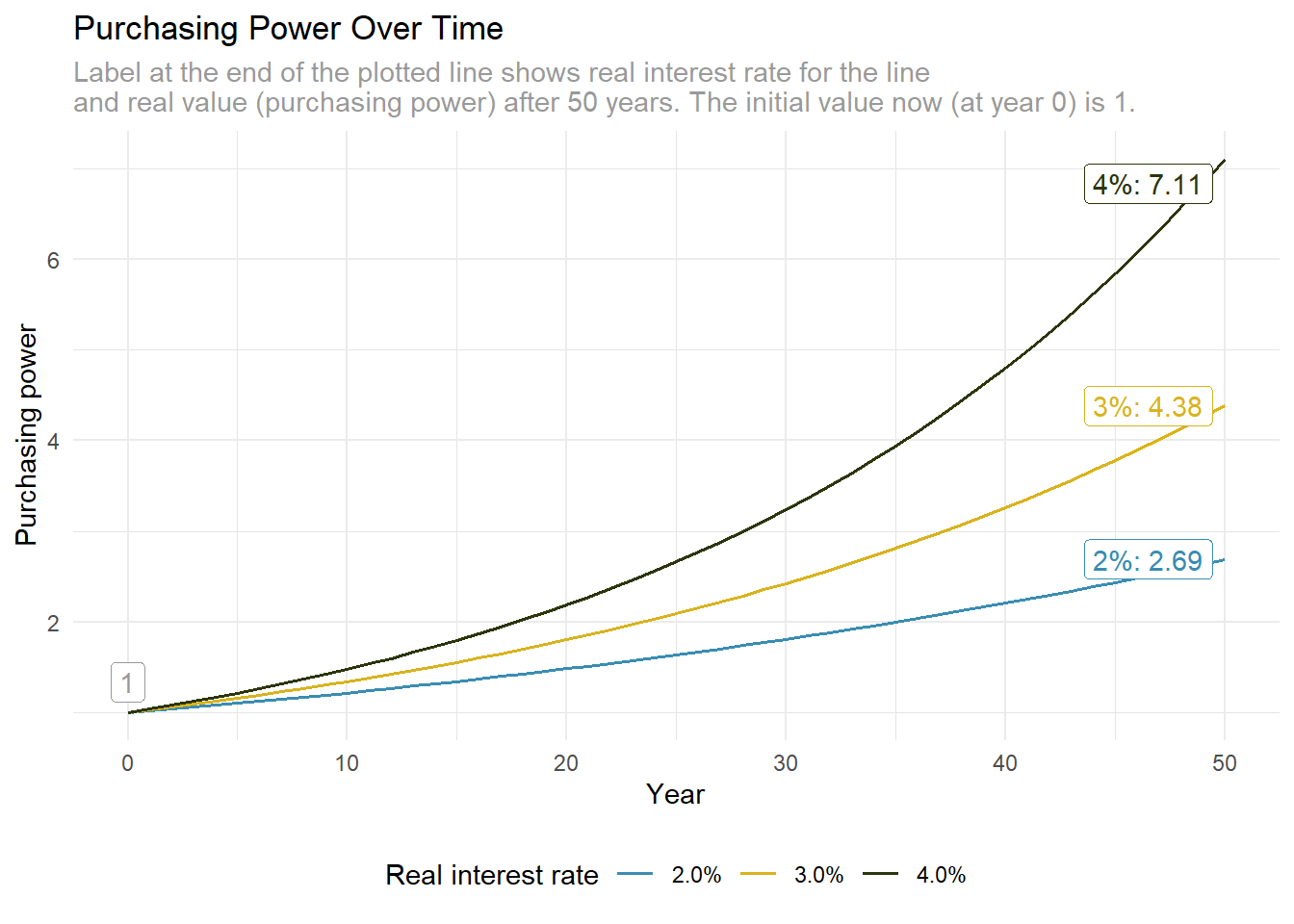

Figure 2 illustrates the impact of compound interest rates over an extended period of time. If Warren Buffett had invested in TIPS with a consistent 4% annual real interest rate starting in 1999, each dollar invested at that time would have appreciated to 2.7 in 25 years and to 7.1 in 50 years. That’s a significant amount.

Figure 2: The purchasing power of a $1 all-bond portfolio over time.

Here’s a simple way to think about compounding: Imagine that with your current savings, as a young individual, you can buy one apple right now. If you were to invest those savings at a real interest rate of 4%, by the time you retire in 50 years, you’d be able to afford seven times more apples. That is a great result, but here’s the thing: Are you really up for waiting around 50 years to finally access that money?

The issue with an all-bond portfolio is that while it may protect our savings from inflation, it fails to offer substantial growth for our invested capital. A 2% real interest rate is considered relatively high, yet the interest rates on bonds available to us fluctuate over time. Even with a steady real interest rate of 2%, we could buy almost three times more apples in 50 years than we can today. This represents a significant boost in your purchasing power, but achieving substantial growth of wealth through compounding interest takes time. The long timeline may not suit everyone’s financial goals, especially if our initial investment is small. Therefore, many of us aim to increase our capital quicker to enjoy a higher standard of living in retirement, or to retire earlier.

Tip

Inflation-protected bonds are the best choice for a safe portion of assets in your portfolio. They shield you from inflation while providing a real return above inflation rates. However, these bonds by themselves do not significantly grow your savings.

You might consider an alternative solution. If bonds, our safe and risk-free assets, are growing slowly, we could shift to something with potentially faster growth (and more risk). This might lead to the idea of investing everything in stocks…

Why you shouldn’t allocate 100% of your investments in stocks?

If someone urges you to invest all your savings in stocks, claiming it will make you wealthy in the long term, should you believe them? More importantly, should you act on that advice?

The argument for investing all of our savings in stocks is that this approach may increase our wealth more rapidly compared to traditional methods like bond investments. Over the long term, a diversified stock portfolio often yields significantly higher real returns over inflation than bonds in long-term. Wealth growth is achievable through the compounding effect of returns. This can be viewed as the reverse of inflation: while inflation erodes the value of our savings over time, compounding interest helps us accumulate more wealth incrementally.

We can invest in the globally diversified stock market by using accumulating ETFs that follow global indices, such as the MSCI World Index or the FTSE All-World Index. Examples of such ETFs include the iShares MSCI World ETF and the Vanguard FTSE All-World UCITS ETF.

Investment influencers often advise concentrating solely on the U.S. stock market, highlighting its historical average annual real return of around 7%. However, it’s crucial to recognize that past performance does not guarantee future results, a detail frequently missed in their recommendations. Influencers also tend to ignore the risks tied to market volatility.

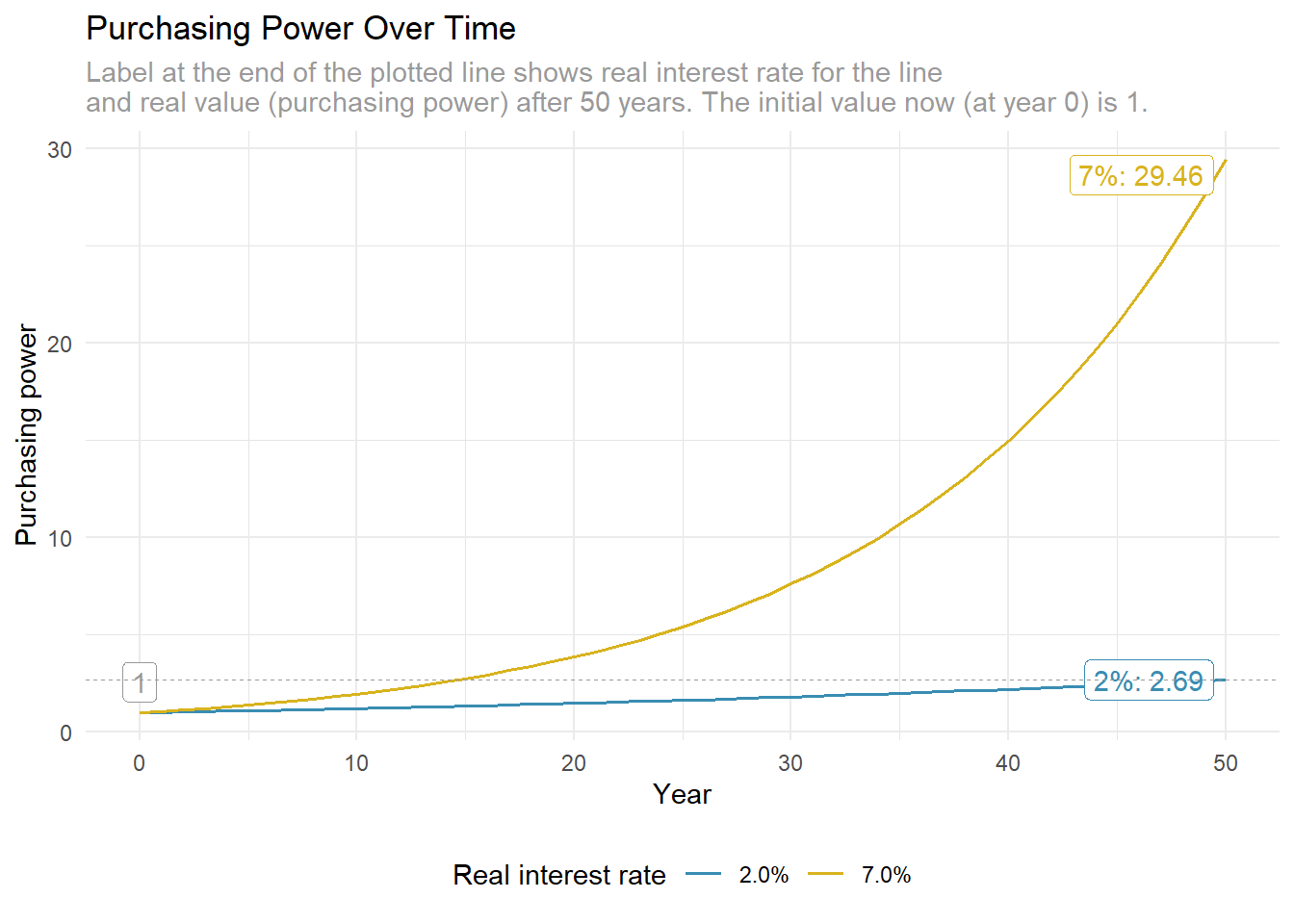

Nonetheless, let’s assume you believe that the future is actually predictable and consider putting all of your money into the U.S. stock market. As shown in Figure 3, the growth rate of a 7% real interest rate is remarkably high! Using the example with apples, were today’s purchasing power allows you to buy one apple. With portfolio of stocks, in 50 years, those same savings could potentially buy you almost 30 apples. Such decision would bring much faster growth compared to bonds, offering a 2% real interest rate, and might yield under 3 apples by the end of the same period. With a 7% interest rate, we would accumulate the same amount of capital in approximately 15 years as we would with a 2% interest rate over 50 years. In long-term the difference would be even more significant. Yeah, let’s forget about bonds and just go all in on the stocks! Well, not quite.

plot_purchasing_power( x =1, real_interest_rate =c(0.02, 0.07))+ggplot2::geom_hline( yintercept =2.7, color ="gray60", size =0.3, linetype ="dashed")

Warning: Using `size` aesthetic for lines was deprecated in ggplot2 3.4.0.

ℹ Please use `linewidth` instead.

Figure 3: The purchasing power of a $1 all-bond with 2% yealry interest rate and $1 stock portfolio with 7% yearly interest rate over time.

There are several issues with adopting an all-in approach to stocks. Many online investment or retirement calculators often assume interest rates remain stable every year. However, this assumption doesn’t hold in real life. Even with a consistent yearly average, the stock market experiences volatility, which is measured by standard deviation—around 15% for the global stock market. Additionally, there can be significant downturns, known as drawdowns, where the value of investments declines from their peak to a subsequent low. Historical examples include the Great Depression, the dot-com bubble, and the 2008 financial crisis.

You can be fairly certain that during your lifetime, you will experience at least one significant drawdown of 50% or more. Based on this, you need to ask yourself a few important questions: What would you do with everything invested in stocks? What if you need to cash out and spend that money, thereby locking in your losses? What if you experience several bad years at the start of retirement, needing to realize losses annually to cover living expenses? This issue, known as the sequence of return risk, could lead to financial difficulty. In a worst-case scenario, you might deplete your resources rapidly, faster then you should, and end up with nothing left.

Keep in mind that you can’t be sure of future average annual stock returns. While they might be around 7%, historical returns don’t predict future returns reliably. They could be higher or lower (more likely lower). In addition to the investment risks, you also experience reduced flexibility if you’re unable to liquidate an investment due to losses that you would incur. You may need to cash out some investments for reasons like taking a sabbatical, changing jobs, starting a business, or pursuing a new direction in life. However, what you really want to avoid is selling depreciating assets at a loss. Unfortunately, you can find yourself completely tied to them, with no other options.

Caution

Globally diversified index funds or ETFs can offer higher average real returns compared to bonds, but they also come with volatility. This volatility represents risk. When taking on risk, it’s crucial to ensure it is the right amount for which you are adequately compensated.

Are you frightened enough? Good. Now, you’re likely reconsidering a full investment in risky assets like stocks, even if they are globally well-diversified. However, you probably still want to grow your savings more quickly, so you can spend on what matters to you in the future. If you’re looking to take some risks to potentially boost your portfolio’s growth, yet still maintain control over your risk exposure, a mix of risky and safe assets might be what you need. The key question now is how much of your portfolio should be allocated to risky assets like stocks and how much to safer assets like bonds?

What portion of my investment portfolio should I allocate to risky assets?

Many popular personal finance authors and bloggers suggest that good asset allocation should allow you to sleep soundly at night. We disagree with this common advice. What if someone can sleep well while being fully invested in extremely risky assets? Such peace of mind might last only until the investment is wiped out completely. The way we manage our savings and how we approach sleep are distinct matters. However, investing our savings wisely could potentially contribute to better sleep. By investing optimally, we might achieve financial peace of mind, which could lead to more restful nights. The question often arises: even if we find the optimal way to invest, what if we cannot stick to it long-term for some psychological reason? Would that mean that we need to change our financial behaviour to a suboptimal or even completely disastrous one, just to make peace with our emotions and instincts? Or maybe we should educate ourselves and work on our reactions, keeping our investment as close as possible to our optimal asset allocation? We believe we could at least start with the former.

Deciding how to structure your investment portfolio is a crucial task. As noted by the authors of the Missing Billionaires:

[…] if you pick bad investments but do a good job sizing them, you should expect to lose money, but your loses won’t be ruinous. You’ll be able to regroup and invest another day. On the other hand, if you pick great investments but commit way too much to them, you can easily go broke from normal ups and downs while waiting for things to pan out (Haghani and White 2023, 4).

What should our optimal asset allocation look like? Should it remain fixed permanently, set in stone?

Fixed vs. Dynamic Asset Allocation

Often, the recommended way is to set a fixed asset allocation (let’s say 60% in stocks and 40% in bonds) and stick to it indefinitely. Is it a good recommendation? Certainly, it’s not the worst recommendation, and it might even be among the best. However, there’s an issue with assuming that allocation principles remain constant over time. This might apply to our level of risk aversion, but what about the actual return rates of our assets?

Fixed asset allocation suggests maintaining the same allocation regardless of actual return rates. Suppose we allocate a portion of our portfolio to safe assets, specifically bonds, which have real returns of 2% above inflation. Now, let’s consider that the expected real returns from the broad stock market are also 2% above inflation. However, the stock market comes with higher volatility, with an annual return standard deviation of about 15%. On the other hand, individual inflation-protected bonds are not volatile at all. So, why would you want to have any portion of your portfolio in risky assets in this particular case? You could be fully invested in these bonds and enjoy a guaranteed real return rate without exposure to risk or volatility. You might argue that the stock market is expected to yield a 7% real return annually. However, by saying this, you’re altering the initial assumption. If investing in a risky asset proves to be more lucrative, relative to the risk involved, your optimal allocation might suggest investing a portion of your portfolio in stocks. But this only holds if the expected returns justify the risk you’re assuming.

Dynamic asset allocation could be even more profitable than static asset allocation, and investing in the global market makes the dynamic approach even more attractive (Haghani and White 2023, 58–59 and p.61). The authors also agree that “[…] it’s better to be a buy-and-hold investor maintaining a fixed exposure to the market than to follow a misguided approach to dynamic asset allocation” (Haghani and White 2023, 64). However, they also convincingly state that “[…] there’s a fundamental flaw in the prevailing conventional advice given to individuals, in which the investor decides how much risk to take based solely on whether they have a ‘high’ or ‘low’ risk tolerance, without factoring in how much they’re being ‘paid’ to take that risk” (Haghani and White 2023, 64). But the authors also conclude that “the next best option [to dynamic asset allocation] is to stick to a static asset allocation comprised of a low-cost global equity index fund with most of the rest invested in long-term TIPS” (Haghani and White 2023, 337).

Tip

The optimal asset allocation should consider both your risk aversion and projections of the real returns on your safe and risky assets. If the projections shift, the optimal allocation of your assets should also adjust.

Due to changes in the world, real return rates are also impacted, which in turn affects your optimal asset allocation. Therefore, your asset allocation shouldn’t be permanently fixed. While fixing it isn’t a poor strategy, it might not be the most optimal one either. It seems logical and sensible to regularly recalculate your optimal asset allocation, perhaps quarterly or monthly, by using updated data on real interest rates. So, how can you calculate this optimal asset allocation?

What do you need to calculate your optimal asset allocation?

To determine your ideal asset allocation, the Merton Share formula is essential. This formula was introduced by Robert C. Merton, a Nobel Prize laureate from 1997. We’ll include the formula below to show its functionality. Don’t worry—we’ll explain its components and provide tools to help you calculate it on your own.

We assume our investment portfolio includes two types of assets: a risky asset class, such as a global stock market ETF, and a safe asset class, such as TIPS or EDO bonds. The Merton share formula calculates the optimal portion of wealth that should be invested in a risky asset. It is defined as follows:

\[

\hat{k} = \frac{\mu - r_f}{\gamma \sigma^2}

\]

To calculate your risky asset allocation—the optimal fraction of wealth invested in the risky asset (\(k^*\))—you need the following inputs:

\(r_f\) — the real return rate of safe, risk-free asset,

\(\mu\) — the expected real return of the risky asset (mean of yearly real returns),

\(\sigma\) — the volatility of the risky asset (standard deviation of yearly real returns),

\(\gamma\) — the risk aversion coefficient.

What are the real returns on your safe asset?

When we use inflation-protected bonds, checking the real returns of currently offered bonds is relatively simple, especially if you are a Polish reader and investor. Visit the official website to find the current fixed rate returns for 10-year individual bonds (EDO) and, if you qualify, the 12-year limited personal bonds (ROD):

If you reside in a different country, it’s important to explore the opportunities for investing in inflation-protected bonds available to you there. If the options are not appealing, you might still consider investing in bonds through an ETF.

Note

In this post, we’ll consider our safe assets as Polish 10-year inflation-protected EDO bonds, which have an annual 2% real interest rate above inflation. Therefore, our \(r_f = 0.02\).

We have successfully identified the real interest rate for our safe asset within the portfolio. However, we must now turn our attention to determining the expected real interest rate for the global stock market.

What real returns of the global stock market could you expect in the future?

Many influencers and popular authors often acknowledge that “past returns are not indicative of future returns.” However, in the same breath, they suggest that because the historical performance of the market has averaged to … (here pick some value between 6% to 12%), we should use this value as an assumption for future returns. This seems contradictory, doesn’t it? If the average real return of the US stock market has been 7% per year, can we expect it to continue like this for the next decade? It might, but it easily might not. We should concentrate on predictive metrics that can reasonably estimate the future real returns of the broad stock market. Our primary interest lies in the global stock market to achieve maximum diversification, given that markets on the Moon or Mars aren’t available yet.

It appears that one specific metric, or a family of metrics, can be particularly useful for making reasonable assumptions about the future long-term real returns of the global stock market.

It is the Cyclically-Adjusted Earnings Yield (CAEY)5. If you haven’t heard about CAEY, you might have heard about CAPE. CAPE is the Cyclically-Adjusted Price-Earnings ratio. 6 And CAEY is just the reciprocal of CAPE (1 divided by CAPE), so \(CAEY = 1/CAPE\).

The CAPE ratio was popularized by Robert Shiller (Nobel Prize in Economic Sciences in 2013) and John Campbell. The CAEY metric was chosen by the authors of Missing Billionaires as a good predictor of future real interest rates for broad stock markets (Haghani and White 2023, 50–51). Later, Victor Haghani and James White introduced a modified version of this metric, PCAEY (Payout and Cyclically-Adjusted Earnings Yield) (Haghani and White 2024b). The new metric explains more variance and seems to have even more predictive power.

It can be surprisingly difficult to locate reliable sources that provide regularly updated metrics available to everyone. This challenge is especially pronounced when seeking updates on the global stock market. Fortunately, the creators of PCAEY have recognized the difficulties faced by even professional investors. As a result, they have recently decided to share these metrics with the public for free and keep them updated (Haghani, White, and Bell 2024).

In the table there, you will be especially interested in the All World Stock Market section and the value at the intersection of the Real Expected Return (PCAEY) row and Yield column (Haghani and White 2024a):

Expected real yearly return for global stock market (PCAEY)

As we want to invest in globally diversified stocks (via ETF or index fund), this is the single number that we are looking for, and we can use it as our assumption of the future real returns for our portfolio’s risky assets.

Note

In this post, we consider our risky asset to be a low-cost global stock index fund or ETF. We use PCAEY metrics as the predictor for real expected return on this risky asset. Consequently, our predicted mean of yearly returns of the global stock market is \(\mu = 0.0449\).

What volatility of risky asset returns could you expect?

Knowing the average annual real return of the global stock market is insufficient. While you may predict an average outcome, each year’s return can vary significantly. One year might yield lower returns than anticipated, while another period could exceed expectations. Over the long-term, the real return is expected to align with the PCAEY metric on average. However, we also need to estimate the variation in yearly returns. To address this, a metric is needed to measure the volatility of the global stock market.

Standard deviation of returns is a crucial measure of risk for assessing risky asset returns. It indicates how much annual returns deviate from the expected average. A low standard deviation signifies that most data points are near the average, whereas a high standard deviation implies a wider dispersion of data points.

The standard deviation as a measure of stock market volatility has its criticism, but we assume that it is a good enough measure for our purposes. Authors of the Missing Billionaires suggest a more complex calculation for the estimate of market risk using a blend of long- and short-horizon realized volatility Haghani and White (2022). We will tackle those issues in more detail in another blog post. In general, we agree with the authors that:

[…] in the case of broad equity markets, a combination of history and theory can give us reasonable ranges for expected returns, variability, and imperfect but still useful techniques for forecasting (Haghani and White 2023, 112).

For now, we approximate our forecast of the standard deviation measure with the historical volatility of a global stock market index. If we take the MSCI World Index (USD), we can see that its volatility, measured by standard deviation, is about 15% in the last 45 years7, which is also in line with what the authors of Missing Billionaires suggest8. We will use it as our good enough approximation of the future volatility of our risky asset.

Note

Our chosen risky asset is a low-cost global stock index fund or ETF. We assume it exhibits a 15% volatility in annual returns, measured by standard deviation. Thus, \(\sigma = 0.15\).

What is your risk aversion?

To estimate the optimal asset allocation, the final piece you need is a numerical value representing your risk aversion. For a typical wealthy investor, a reasonable default value is 2(Haghani and White 2023, 42).

If we have a risk aversion of 2, it indicates that we are moderately risk-averse. This means we consider ourselves fairly cautious in taking risks but are still open to risking some of our wealth for the opportunity to increase it. This value indicates that we are neither risk-neutral nor risk-seeking, which most of us are not and should not be. A coefficient of 1 might suggest a higher expected wealth growth rate. However, it also implies an excessive tolerance for risk, which is generally unacceptable for most people (Haghani and White 2023, 113).

Later, you will be able to calibrate this value and increase it if you are or become more risk-averse. “For the vast majority, their coefficient of risk-aversion fell within a fairly tight range of 2-3” (Haghani and White 2023, 107). Still, a risk-aversion level of 2 is generally considered a reasonable default for many wealthy investors. What do we mean by wealthy investors? In this context, and for now, we can define wealthy investors as those who invest long-term and only savings that are not needed in the near future. This is because our risk aversion could be much higher if we can barely cover the most essential needs (Haghani and White 2023, 179).

This single value represents your personal or your household’s collective risk aversion. Typically, it remains stable over time. However, it may change in the long term. For instance, after accumulating sufficient capital near or after retirement, you might become more risk-averse. This shift will then influence your optimal asset allocation.

Note

Our risk-aversion coefficient is set to 2, so \(\gamma = 2\).

Calculate your optimal allocation

We can now apply the Merton Share formula to determine our optimal allocation in risky assets.

\[

\hat{k} = \frac{\mu - r_f}{\gamma \sigma^2}

\]

To do this, we’ll use the reasonable default values we previously discussed:

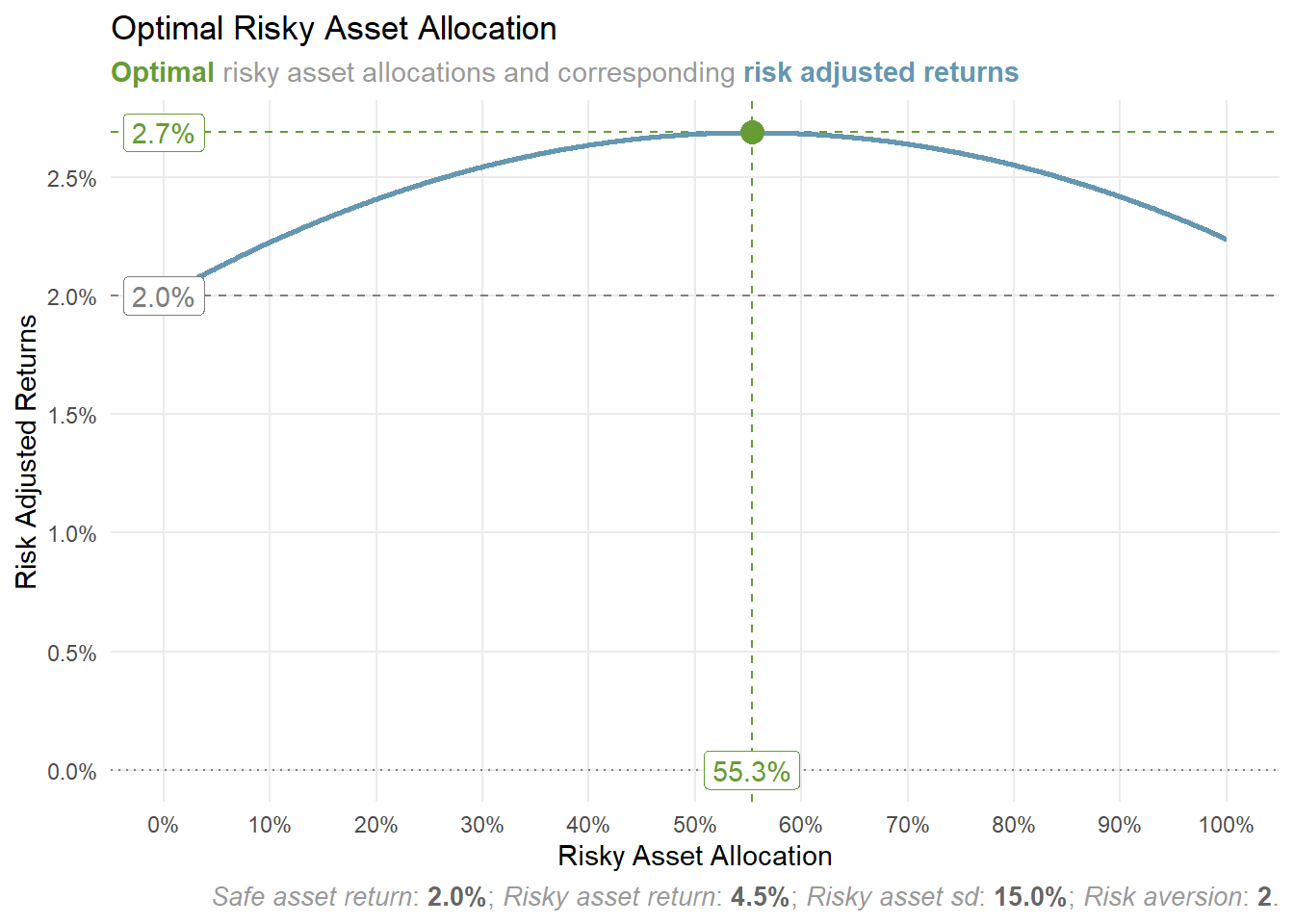

And there it is! The key ratio for nailing optimal asset allocation. Given the inputs available at the moment of writing this post, we should invest in our risky assets based on the global stock index, 55.3%. The rest of our portfolio (44.7%) would be in safe assets (in our example, that means Polish EDO 10-year bonds).

What should you do if your current allocation differs from the optimal one?

Once you’ve determined your optimal allocation to a risky asset, the next step is to assess your current risky asset allocation. This allows you to see how it compares to the optimal allocation and determine the necessary adjustments.

How to calculate your current risky asset allocation?

If your portfolio follows the structure of the ones in our earlier example and includes \(asset_{safe}\) (Polish EDO Bonds in our example) and \(asset_{risky}\) (ETFs tied to a global stock market index), you should add the current value of your safe assets (bonds) and your risky assets (ETF). Then, determine what percentage of the total portfolio is allocated to the risky asset.

\[

k = \frac{asset_{risky}}{asset_{risky} + asset_{safe}}

\]

You may have noticed that your current risky asset allocation differs—either lower or higher—from your optimal allocation. If that’s the case, what steps should you take? Is it necessary to rebalance your portfolio and shift immediately to your optimal allocation?

Should you switch to your optimal allocation immediately?

From a purely mathematical perspective, you should try to achieve optimal asset allocation as soon as possible. There is no point in remaining in a suboptimal state (and, for example, bearing too much risk or not enough) if we could easily transition to our optimal state:

“[…] cold logic dictates that we should immediately move our allocation to the optimal point, minimizing the amount of time spent at a suboptimal allocation […] any approach other than moving straight to your optimal allocation is financially suboptimal. However, some plans are less suboptimal than others […]” (Haghani and White 2023, 85–86).

If you have an efficient method to quickly achieve your optimal asset allocation, it’s advisable to implement it swiftly and in one move. However, this process is often challenging. Transitioning to your optimal allocation can involve rebalancing costs, transaction fees, brokerage expenses, and capital gains taxes, among other factors.

Furthermore, rebalancing too frequently can lead to incurring costs without gaining significant benefits in terms of risk-adjusted returns. Why is this the case?

How much risk is enough?

Remember the problem where we were considering whether to buy a risky asset that has the same real return as a safe asset? We concluded that it doesn’t make sense because the risky asset inherently carries more risk. Therefore, you’re not adequately compensated for the extra risk by choosing the risky asset. But how to know if you are compensated enough for the extra risk you are taking?

The risk-adjusted return is a useful metric for evaluating how much return you obtain in relation to the risk you take. This metric adjusts raw returns by reducing them based on the level of risk; the higher the risk, the lower the risk-adjusted returns. Your aim should be to maximize these risk-adjusted returns by correctly allocating a portion of your investment portfolio to risky assets.

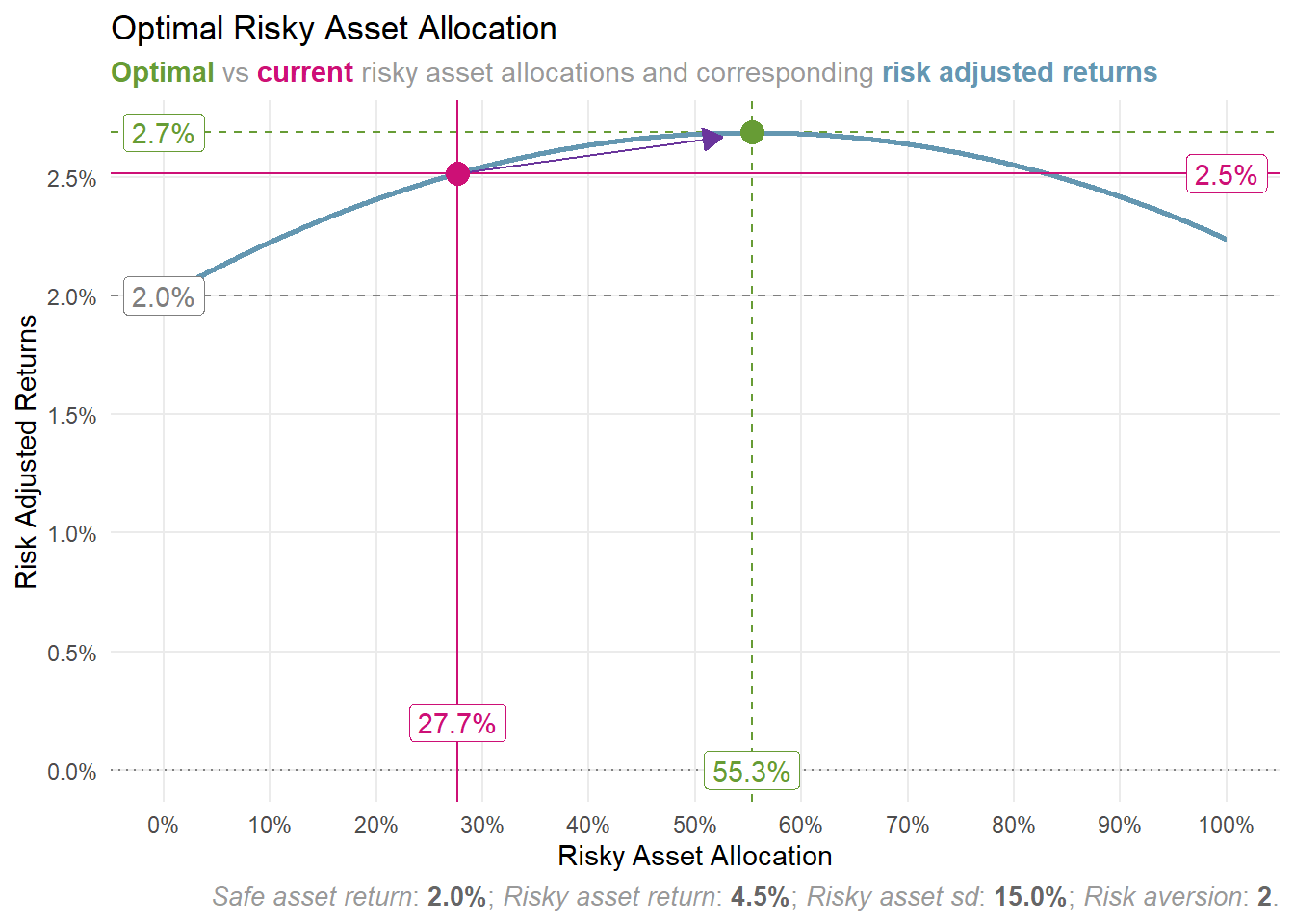

Refer to Figure 4. This figure shows the impact of risky assets allocation on Risk Adjusted Returns. You will see that as risky asset allocation rises, Risk Adjusted Returns improve —– but only up to the optimal allocation point. Beyond this point, Risk Adjusted Returns start to decline. The other thing to note is that the risk-adjusted returns rise more swiftly when you are far from the optimal allocation of risky assets. In contrast, the increase is much slower when you’re close to the optimal level. Furthermore, if you exceed your optimal asset allocation, the decline in risk-adjusted returns starts gradually, but then accelerates rapidly.

Keep in mind that there is an optimal level of risk that yields the highest risk-adjusted returns.

Taking on too little or too much risk is not optimal.

Examine now Figure 5. Notice that without any allocation to the risky asset if you move from 0% allocation halfway to your optimal allocation, or 27.7%, it will give you a rise in risk-adjusted returns from 2% to 2.52%. This is already 75.4% of the benefits (up to a maximum of 2.69%) with only 50% towards your optimal risky asset allocation. As the authors of Missing Billionaires noticed, it’s one of those few times that \(1/2 = 3/4\)(Haghani and White 2023, 85). And it works to our advantage, as 50% in efforts gives you 75% in benefits!

Figure 5: Moving from 0% risky asset allocation halfway to your optimal allocation (27.7%) gives you 3/4 of the benefits (from 2% to 2.5% risk-adjusted returns, up to a maximum of 2.7%).

It’s still beneficial to move closer to your optimal risky asset allocation as the risk-adjusted return will still rise a bit, but it will rise slower and slower. “Decisions that are in the general vicinity of optimality will give you nearly all the benefits of going all the way to the hypothetically perfect spot” (Haghani and White 2023, 338).

Tip

Achieving the optimal asset allocation yields the best results.

However, being “close enough” to optimal asset allocation already provides most of the advantages!

The crucial point, however, is that exceeding your optimal risky asset allocation leads to diminishing returns. Initially, moving slightly above your ideal allocation isn’t significantly problematic. However, going much further reduces the benefits you previously achieved.

You could allocate 100% of your portfolio to risky assets, but in terms of risk-adjusted returns, this would be comparable to having only about a 10% allocation in risky assets (both allocations 10% and 100% gives the same risk-adjusted returns of about 2.2%). This 100% allocation strategy is far from optimal, as you’ll take on significantly more risk than you actually need to achieve the same Risk-adjusted Returns as with 10% allocation (see again Figure 5).

But the most important lesson here is that taking too little or too much risk doesn’t make sense, and “taking twice the optimal amount of risk completely wipes out the risk-adjusted benefit of a good investment, and taking more risk than that makes you exponentially worse off than doing nothing at all” (Haghani and White 2023, 335).

Caution

Doing nothing could be a better option than taking on too much risk beyond your optimal risky asset allocation.

Being near an optimal allocation provides most of the benefits. If you’re significantly far from it, that’s a concern, and you should try to be closer. However, if you’re already close, small deviations don’t matter much. Nonetheless, if you’re going to buy or sell within your portfolio, aim to move your asset allocation toward the optimal level. Here are a few simple rebalancing rules you can follow to achieve that.

Which rebalancing rules should you follow?

If you’re looking to buy or sell something from your portfolio while staying close to your optimal allocation, you should follow these guidelines:

Tip

If you current risky asset allocation is lower then the optimal one:

if you need to sell — sell safe asset.

if you want to buy — buy risky asset.

if you wish to rebalance — sell safe asset and buy risky asset.

If you current risky asset allocation is higher then the optimal one:

if you need to sell — sell risky asset.

if you want to buy — buy safe asset.

if you wish to rebalance — sell risky asset and buy safe asset.

What if something drastic changes in the economy?

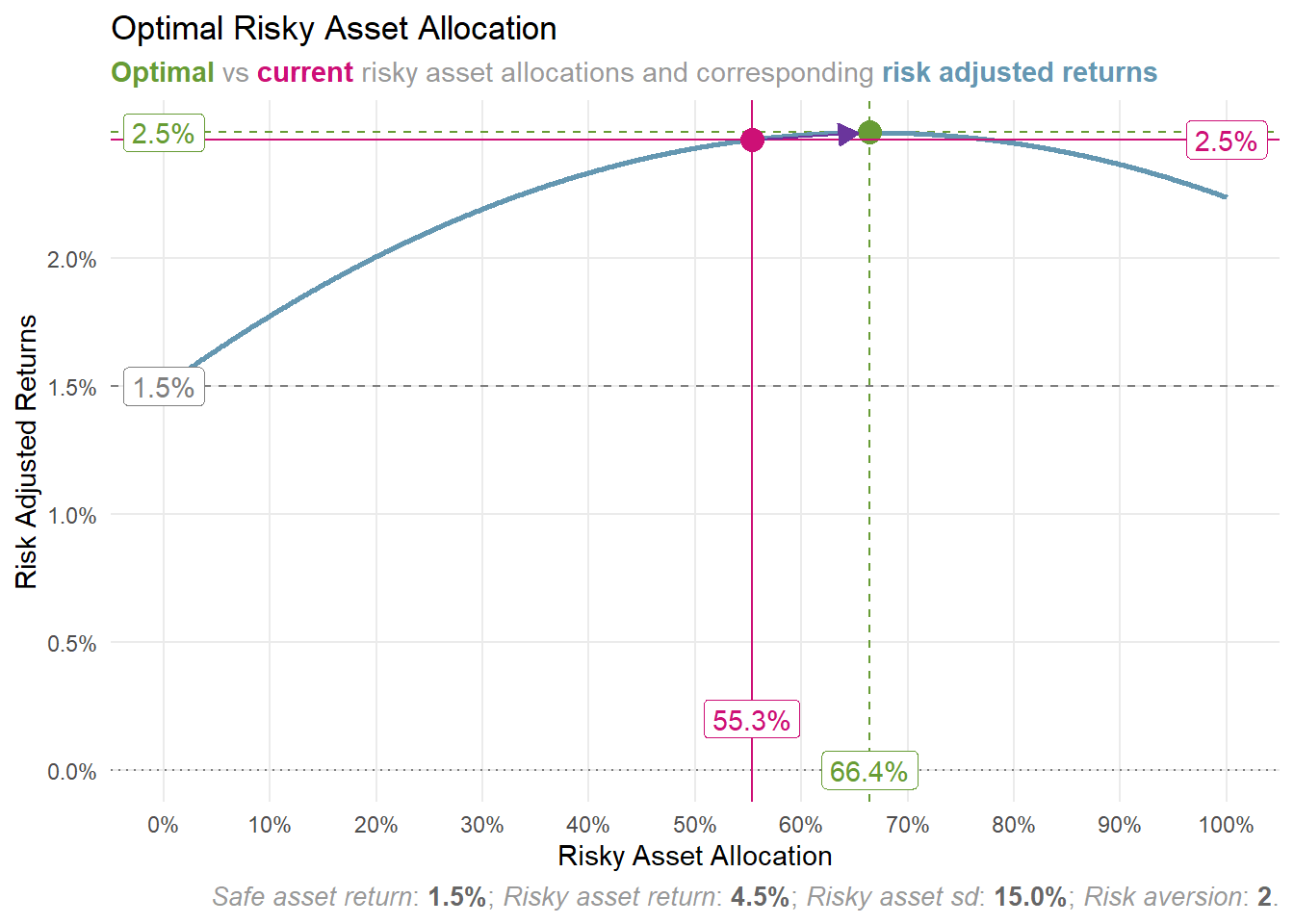

Since economic conditions can fluctuate, our ideal asset allocation isn’t permanent and can evolve over time. For instance, if the real return rates of our EDO bonds decrease from 2% to 1.5%, our optimal asset allocation could adjust from the previous 55.33% to 66.44%. Why does this happen? With the reduced returns of the secure assets, the riskier option becomes more appealing given it offers the same returns and volatility.

Figure 6: Impact of safe asset return change from 2% to 1.5% on optimal risky asset allocation

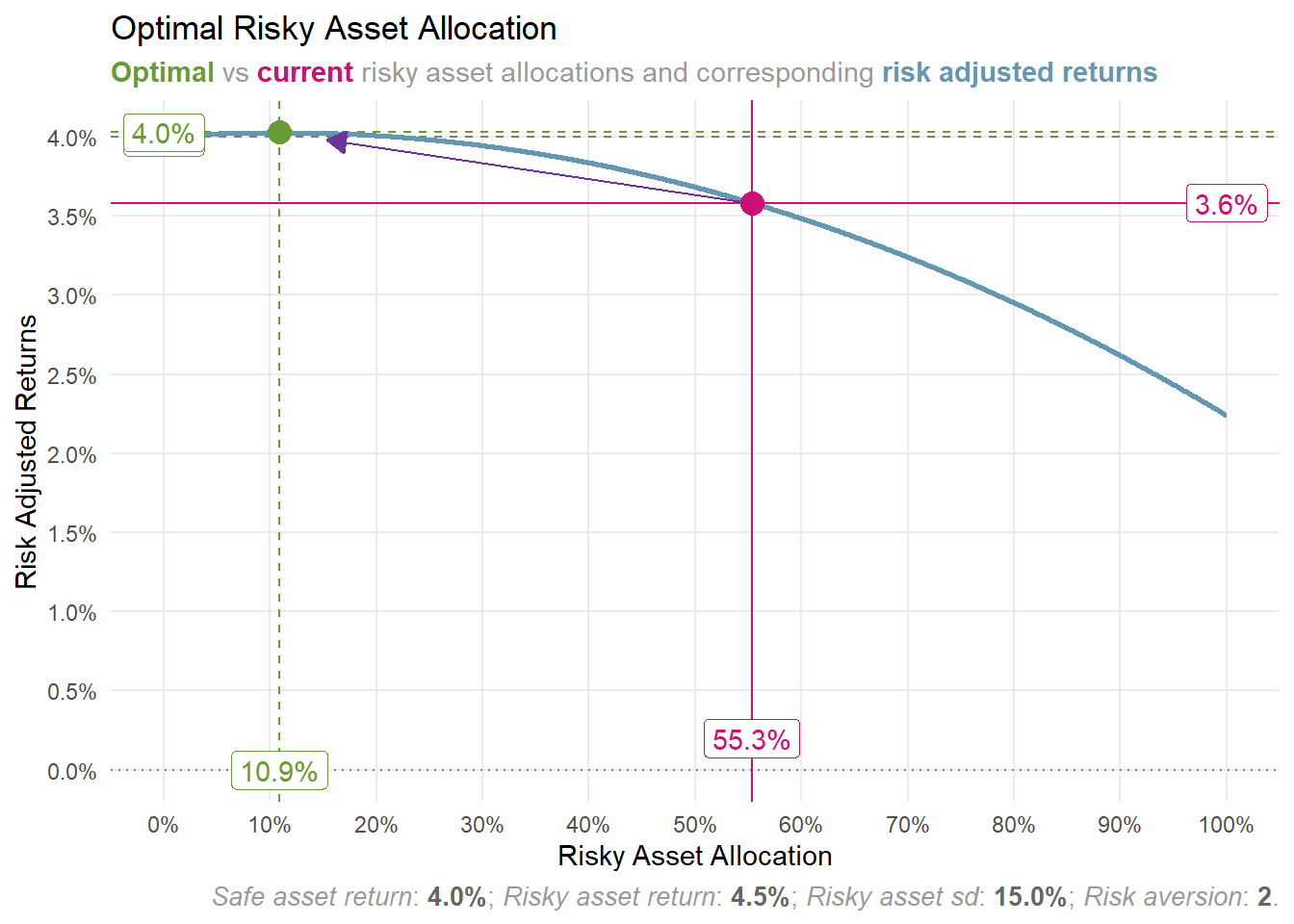

If we consider the possibility of the bond’s real interest rate increasing to 4% (similar to TIPS in 1999), our optimal allocation for risky assets would sharply decrease to 10.89%. This is because risky assets would be much less appealing compared to the attractive interest rates of safer options (see Figure 7).

Figure 7: Examining the effect of an increase in safe asset returns from 2% to 4% on the allocation to risky assets.

In practice, expect that the inputs to the Merton Share formula will vary over time. This variability is anticipated. When these changes occur, update the model accordingly and rerun the calculations. Then, determine your revised optimal asset allocation and consider steps to achieve this new target.

Can I check the optimal risky asset allocation in different scenarios by myself?

Certainly! There are three ways to achieve this:

Manually calculate the optimal risky asset allocation by inputting the updated values into the Merton Share formula.

Explore our interactive web app, which computes the optimal risky asset allocation and generates a Risk Adjusted Returns plot based on your input.

Important

The R package will soon be available to the public. When we release the R4GoodPersonalFinances package, we’ll also add an interactive app to our website. This app lets you test different inputs to the Merton Share formula on your own. Stay tuned for updates; we will inform you here on this post and through our newsletter.

We will occasionally update this article, refreshing our calculations and plots with the latest real return data.

Conclusions

If you’ve ever wondered, like we have, if there’s a straightforward and effective way to invest your hard-earned savings, you should check out the Merton Share formula. It’s a great tool for figuring out the best asset allocation for your investment portfolio.

Even if you have an idea about alternative ways to manage your money, you can still use the approach mentioned above as your baseline. Consider it your benchmark to compare other investment strategies against.

However, it’s likely you’ll soon realize how tough it is to find a strategy that’s better. The challenge lies in finding one that’s simple, easy to maintain over time, and efficient, without taking on too much risk. For the risk you do take, it ensures you’re properly rewarded. Plus, it’s not just about picking the right assets. It’s also about investing the right proportion of your money into them.

Tip

Steps to follow when you have some extra cash ready for investment:

Check if the inputs to the Merton Share formula have changed since your last review. Update them if needed.

Calculate your optimal risky asset allocation using the Merton Share formula. Use the updated inputs.

Calculate your current risky asset allocation.

Decide whether to put your money into safe or risky assets.

Choose the option that brings your current risky asset allocation closer to the optimal level.

If you’re living off your savings, like during retirement or between jobs, use the same decision process before choosing which assets to sell.

It may be beneficial to review this process monthly, similar to what we do, regardless of whether you have extra cash to invest or a need to sell assets. Avoid conducting these reviews more frequently, but you can opt to do them less often if preferred. The objective is to assess whether your asset allocation remains near its optimal level and to consider rebalancing if needed.

After checking out this article, you should feel pretty confident about catching some good night sleep:

You understand how to manage your asset allocation effectively.

You’re aware of the steps to maintain it close to optimal.

You realize that constantly seeking the perfect asset allocation isn’t necessary.

You know how to determine how much to invest in a risky asset at any time, with default reasonable settings.

Topics to study further

Here is a list of topics that could be further explored. Please let us know if any of these subjects particularly interest you. Feel free to send us an email or leave a comment. We consider the following topics valuable for future exploration. If you have any additional ideas, please share them with us.

How can you calibrate your personal or household risk aversion? Does it vary with changes in wealth or age? Should it?

What are the top candidates for our safe and risky assets, particularly among bonds and ETFs?

A deep dive into CAPE, CAEY, and PCAEY examines their effectiveness in predicting real returns in the global stock market.

Explore inflation-protected safe assets to assess their effectiveness against varying inflation rates. Focus particularly on country-specific options like Polish EDO bonds. Consider individual inflation rates.

Understanding Risk-Adjusted Rates and Certainty-Equivalent Return Rates.

Understanding the risk of sequence of returns.

How does a stock market crash should affect our asset allocation?

How can we factor in human capital when optimizing asset allocations? Should optimal asset allocation strategies be adjusted as we age?

An In-depth Comparison of Dynamic vs. Static Asset Allocation.

Methods for estimating volatility of the global stock market.

In our upcoming blog posts, we plan to address some of these topics. Additionally, we’ll update you on new content through our newsletter. Subscribe to stay informed.

Try our interactive web apps

Tip

You can use your own customized inputs with our interactive web apps, that can be found on the Tools page.

See for yourself how different real interest rates affect purchasing power over time, or if your current risky asset allocation gives you the highest risk-adjusted returns possible and thus is optimal for you.

TreasuryDirect. Comparison of TIPS and Series I Savings Bonds https://www.treasurydirect.gov/research-center/history-of-savings-bond/comparing-tips-to-i/↩︎

“When the CAPE ratio is high, investors are paying a high price for a normalized stream of earnings, and the prospective return of the stock market is low” (Haghani and White 2023, 50)↩︎

DISCLAIMER! The content on this blog is provided solely for educational purposes. It does not constitute any form of investment advice, recommendation to buy or sell any securities, or suggestion to adopt any investment strategy. Any investment strategies and results discussed herein are for illustration purposes only.

The content reflects the observations and views of the author(s) at the time of writing, which are subject to change at any time without prior notice. The information is derived from sources deemed reliable by the authors, but its accuracy and completeness cannot be guaranteed. This material does not take into account specific investment objectives, financial situations, or the particular needs of any individual reader. Any views regarding future outcomes may or may not materialize. Past performance is not indicative of future results.

This content is not investment advice or information recommending or suggesting an investment strategy within the meaning of Article 20(1) of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse.

Investing always involves risks, and any investment decisions are made at your own responsibility.